Whether you’re 55 with nothing saved or 62 with something — the most important step is the one you take next.

Most people spend more time planning a holiday than they do planning the last third of their life. That’s not a criticism — it’s just where most of us end up. Life fills in around you: a young family, a mortgage, a career that demanded everything you had. And then one day you look up and realise that retirement isn’t a distant concept anymore. It’s the next thing on the list.

If you’re reading this and feeling behind — maybe significantly behind — the first thing to understand is that you are not the exception. You are, in fact, in very good company. But that doesn’t mean staying there. What it does mean is that the path forward looks different from here than it would have at 35, and it requires a different kind of focus.

This post is for the people who are ready to face it clearly. Not with panic, and not with false optimism — but with a calm, honest look at where you are and what’s actually within your reach.

Start with your timeline, not your regrets

Before anything else, you need to know your runway. Not in a frightening way — in a practical one.

If you’re 55 and in reasonable health, you likely have ten years before the conventional retirement age and fifteen or more before the age most financial plans now run to. That is a meaningful amount of time. It is enough time to change your trajectory substantially, provided you stop treating it as abstract and start treating it as finite.

The single greatest financial asset most people have in this window isn’t their savings account — it’s their income. The ability to earn, to redirect, to make deliberate choices about where money goes. That capacity, used with intention, is more powerful than most people give it credit for.

“That what each of us calls our necessary expenses will always grow to equal our incomes unless we protest to the contrary.” — George S. Clason, The Richest Man in Babylon

The protest Clason is describing is not deprivation. It’s a decision. And decisions require information.

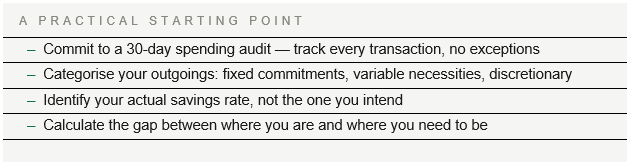

Know your numbers — actually know them

This is the section most people skim, because it sounds straightforward. It isn’t. Or rather, it’s simple in theory and quietly avoided in practice.

Knowing your numbers means understanding, with precision, what comes in each month and what leaves. Not approximately. Not a rough sense. The actual figures. If you haven’t done this in a while, the results tend to be surprising — and not always in the direction people expect. There are usually places where money has quietly been disappearing that, once visible, are easy to address.

The word ‘budget’ carries a lot of uncomfortable weight for many people. It sounds restrictive — like a diet you can’t sustain. But a budget isn’t a constraint. It’s a map. And you can’t navigate without one.

The people who tend to build the most security by retirement are rarely the highest earners in any room. They are the people who know, at any given moment, exactly what they’re doing with what they have. Income level is far less predictive than awareness.

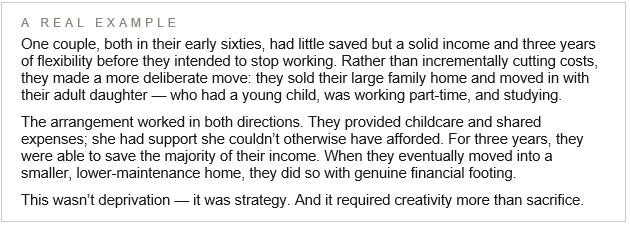

Think creatively about your cost of living

Once you have clarity on your numbers, the next question is where there is room to move. For many people approaching retirement, the most significant lever isn’t investment returns — it’s expenditure. Specifically, whether there are structural ways to reduce it meaningfully, even temporarily.

Not everyone will do something this dramatic, and they don’t need to. But the underlying question is worth asking: what would it look like to significantly reduce your cost of living for two or three years? What becomes possible if you do?

Downsizing, renting out a room, relocating somewhere less expensive, consolidating households with family — none of these are failures. They are options, and options are what you’re looking for.

Reconsider what retirement actually means

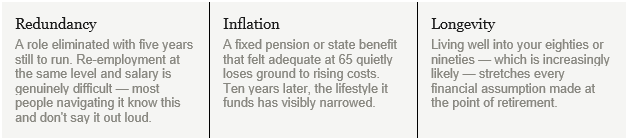

The idea that retirement happens at a fixed age — full stop, no income, indefinite leisure — is increasingly outdated. It was built around a life expectancy that no longer applies to most people in good health. If you and your partner are both in your early sixties, there is a meaningful statistical probability that one of you will live into your nineties. Planning for that isn’t pessimism; it’s arithmetic.

Working a few years longer, if it’s financially and physically viable, has a compounding effect that is difficult to overstate. It means more years of contributions, fewer years drawing down, a stronger pension position, and more time for whatever savings you have to grow. Even a shift from full retirement to part-time work can extend financial runway considerably.

There’s also a separate question worth sitting with: are you tired of your job, or tired of that particular version of working? Some people who retire find, within a year or two, that they want to return to some form of meaningful work — not because they have to, but because the structure and purpose were more valuable than they’d realised. If that’s a possibility for you, it’s worth factoring in before you make decisions that are difficult to reverse.

The option most people don’t put on the table: build an income that doesn’t stop when you do

There’s an assumption buried quietly inside most retirement planning — that income is something your employer provides, and that when the employment ends, the income ends with it. For a generation that largely lived that way, it felt like a natural law. It isn’t.

There is a different way to think about this, and it becomes particularly compelling for anyone who finds themselves approaching retirement with less saved than they’d like, or anyone navigating one of the scenarios that tend to blindside people in their late fifties and sixties.

What these three scenarios share is that they are all problems of income. And the most direct solution to a problem of income is to build one that isn’t dependent on any single employer, any fixed rate, or any arbitrary retirement age.

A small, well-run business — one built around skills, knowledge, or experience you already have — can do something that a pension cannot: it can grow. It can respond to inflation because you set the prices. It can continue generating income for as long as you choose to run it, with as much or as little involvement as suits your life at any given point.

And it changes the entire relationship between you and your state or national pension. When your income doesn’t depend on it, it becomes something else entirely — a bonus, a buffer, a fund for the things that genuinely matter to you, rather than the financial floor you’re surviving on. The difference between a pension you need and a pension you’re banking is the difference between constraint and choice.

When your pension becomes optional rather than essential, it stops being a ceiling and starts being a gift you give yourself every month.

This isn’t a call to throw yourself into entrepreneurship recklessly, or to put your retirement savings at risk in a venture you haven’t thought through. It’s a suggestion to put it on the table as a serious option — one that deserves the same honest evaluation as downsizing your home or working a few additional years.

We’ll be going deep on this in future posts: what kinds of businesses tend to work well for people in this phase of life, how to start without significant capital, how to structure it around the rest of your commitments, and how to avoid the mistakes that cost people time they don’t have to waste. If this thread interests you, it’s worth staying close to this series.

Your health is a financial decision too

This point gets left out of most retirement planning conversations, which is a genuine oversight. The cost of poor health in later life — medical, pharmaceutical, care — is one of the largest and least predictable expenses people face. It is also, within limits, one of the most preventable.

Staying physically active, eating well, and managing stress aren’t just quality-of-life decisions. They are, in a direct and measurable sense, financial ones. The capacity to work longer, to remain independent, to avoid expensive interventions — all of it is shaped by choices made now. This isn’t a health lecture; it’s a planning point.

The most important thing you can do today

It’s not to open an investment account. It’s not to call a financial adviser. It’s to spend thirty days finding out, with complete honesty, exactly where your money goes.

Everything else follows from that. The decisions about what to cut, what to redirect, whether to work longer, how to structure your later years — all of it becomes possible once you can see your financial life clearly. Without that visibility, you’re planning in the dark.

You are more capable of navigating this than you may currently believe. But capability without information is difficult to apply. Start with the numbers. The rest has a way of becoming clearer from there.

This is a pillar post in the Your Retirement Business series on financial clarity for people approaching or reconsidering retirement. Future posts will explore specific strategies for income generation, building a retirement business, and creating financial resilience later in life..